ALERTE | Ce site est en cours de mise à jour. Certaines informations seront ajoutées après les Fêtes. La version anglaise sera disponible au début de 2026.

NOTICE | This website is currently being updated. Some information will be added after the holidays. The English version will be available in early 2026.

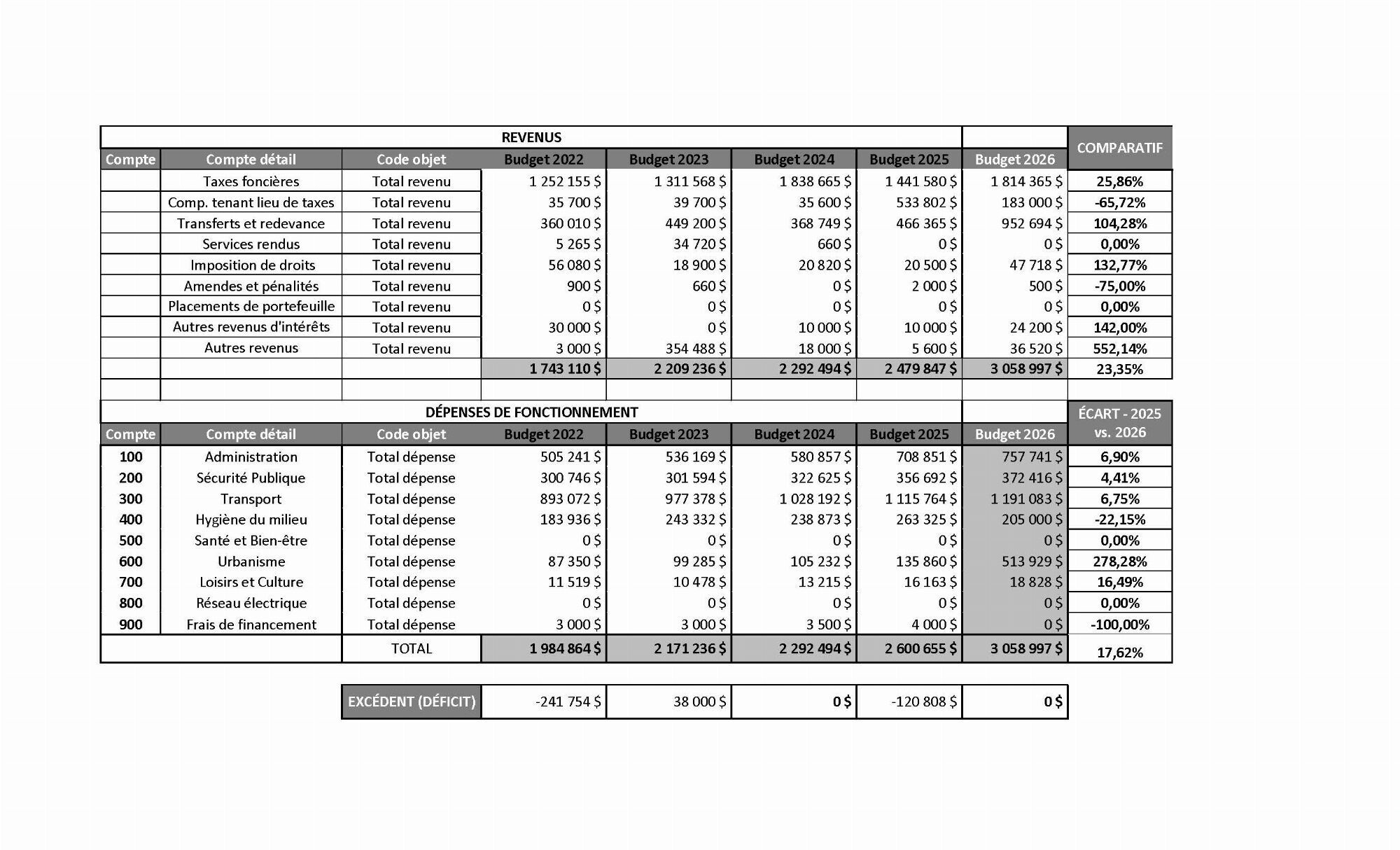

Elected officials are responsible for setting broad directions, defining priorities, and making key decisions in order to meet the needs expressed by citizens.

These broad directions are then shared with the administration so they can be integrated into the budget. The administration prepares the budget with the participation of all departments and presents it to elected officials for approval.

This process is the key to municipal service planning, as it allows the municipality to determine the services offered to citizens and estimate their cost, identify funding sources, and calculate applicable tax rates for taxpayers.

The CIP is a municipal budget planning tool that sets out planned investments in infrastructure and assets (roads, buildings, parks) over a three-year period. Updated annually, it details the timeline, costs, and funding methods for projects.

Thr key elements of the CIP include:

Objectives: Plan development priorities, assess financial impact on the annual budget, and plan borrowing by-laws.

Content: Infrastructure projects (road rehabilitation, water infrastructure, sports facilities, parks) including their amounts and funding sources.

Process: It is adopted annually by the municipal council, usually in December, and serves as a roadmap for the next three years.

Importance: Essential for asset maintenance and long-term public finance management.

The CIP enables better management of financial resources and the municipality's development priorities.

A capitalization policy for capital assets defines the accounting rules for recording the acquisition or improvement of an asset as a long-term asset on the balance sheet, rather than as an immediate expense. It is based on a capitalization threshold (minimum amount) and a useful life (generally more than one (1) year), allowing the cost to be allocated over time through amortization.

-